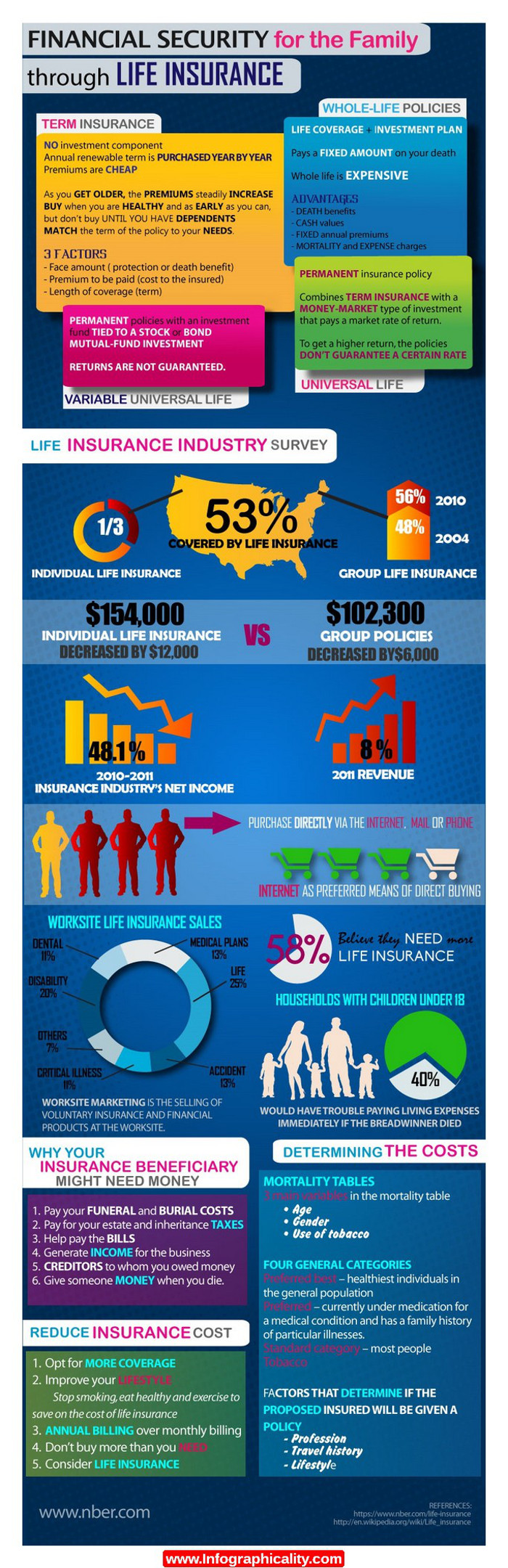

Not like other forms of universal life insurance available, variable universal life insurance permits policyholders to put in cash value of the policies in diverse accounts such as commodities, bonds and stock the same as the mutual funds. Owners of the policy can put in all their money in one account, or put in the cash in many different accounts in order to make the most of the ROI.

Like every life protection, client must consider the pros and cons of variable universal life insurance prior to deciding the kind of coverage which is appropriate for their necessities. After understanding about the various kinds of policies and knowing the most excellent coverage for the family, assess rates with life insurance estimate to get reasonable options and company.

Pros of Variable Universal Life Insurance Coverage

1. Flexible: Not like level term and whole life insurance that have stable payment, variable universal security has flexible payment with a maximum and minimum payment. A fraction of the payment disburses for the insurance and the remaining balance is abstracted to investment accounts, developing the cash value of the policy. The higher payment you disburse, the quicker the cash worth and the investment grows. If the person insured is not capable to make payment, this policy allows the disbursement to be done through withdrawing the payment from the value of cash, so the coverage doesn’t lapse and remain standing.

2.Tax Advantage: The returns obtained in the life insurance cash value are tax deferred prior to withdrawal. Through utilizing the value of cash for no interest mortgages, the insured individual can prevent paying taxes. The only warning in the tax deferred is that when the mortgages equal the value of the cash amount, the coverage lapses and the income taxes appear due in lump sums that can be essential.

Cons of Variable Universal Life Insurance

1.Riskier Investment: Except the coverage has least assured percentage of return, the person insured can lose the investment because the monetary instrument utilized to make profit also have the possibility for loss. Even as some complete life policy assures an inexpensive and safe return, the rate of the return on this policy can be as low as 2 percent. If the expenses related with the account are subtracted, the ROI of person insured might be nothing for the whole year.

2. Costs: The Term life insurance is impermanent security without value and it provides reasonable rates that are lower compared to this kind of life insurance or any kind of policy. On the other hand, variable universal life insurance is more reasonable compare to other type of permanent policy. For parents, adults and seniors who just need or want security for monetary dependent, the term life provides the lowest rates.

Always remember variable universal life unites with insurance coverage with investment car and the cost reflects the two nature of insurance policy. For those who are searching for means to have a secure retirement or want to enhance their asset, this policy provides the best coverage.

It is essential to weigh the pros and cons of variable universal life insurance policy prior to applying in order to avoid regret in due course.